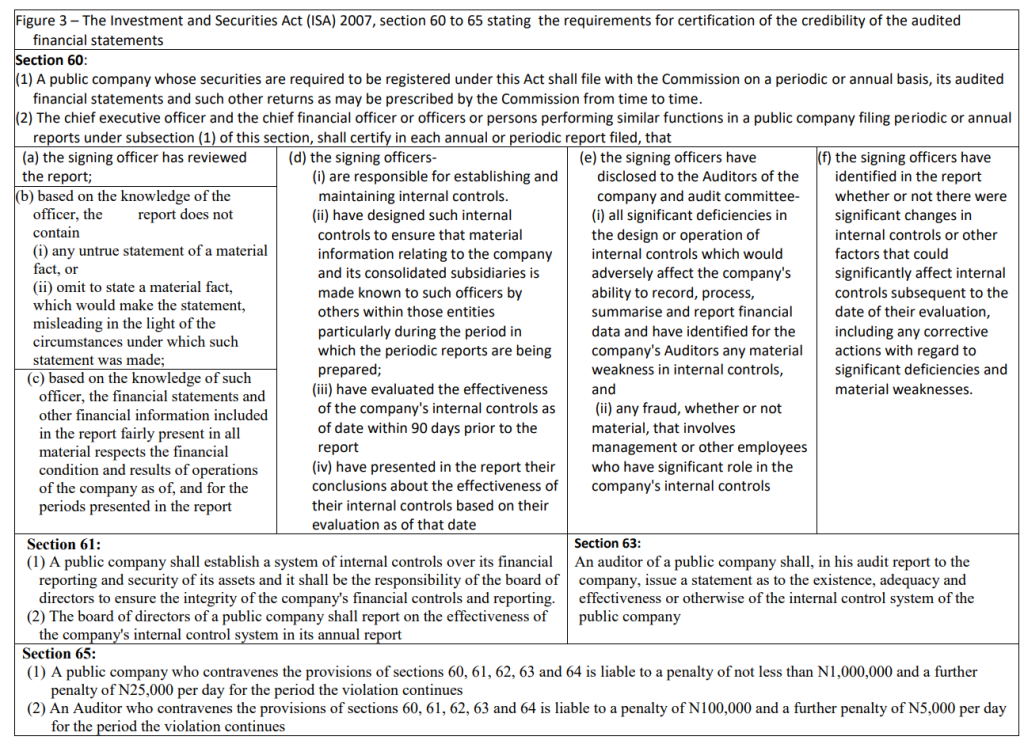

What Exactly Are the Specific Requirements for The Certifications on Financial Statements?

From the perspectives of the Investment and Securities Act 2007, the details of the specific tasks that the Chief Executive Officer and Chief Financial Officer should do to make the certification on the credibility of the financial statements have been presented in figure 3 below:

The Attestation requirement of the statutory auditor requires the statutory auditor to issue a statement as to the existence, adequacy and effectiveness or otherwise of the internal control system of the public company.

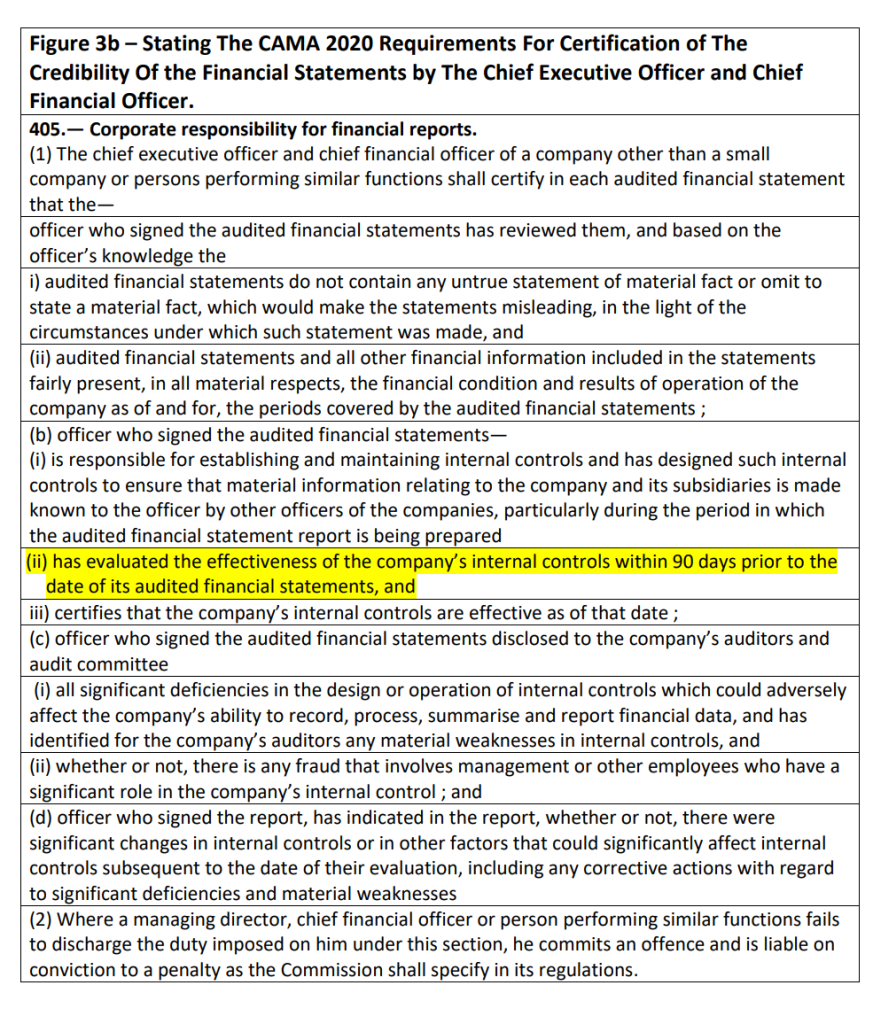

CAMA 2020 and FRC Act 2011 shares the same perspectives with the ISA 2007 section 60 pronouncement on the composition of the certification requirements and also section 65 on the Attestation requirements. Presented in figure 3b below are the specific certification requirements prescribed by CAMA 2020 for the Chief Executive Officer and Chief Financial Officer.

Furthermore, CAMA 2020 section 404 (7d) states that the objectives and functions of the audit

committee are to keep under review the effectiveness of the company’s system of accounting and internal control.

Thank you for this insightful post. And thanks for creating awareness as some companies are not even aware of the the immense benefits of ICFR

Thank you for free lecture.

Great write up…simply explained.