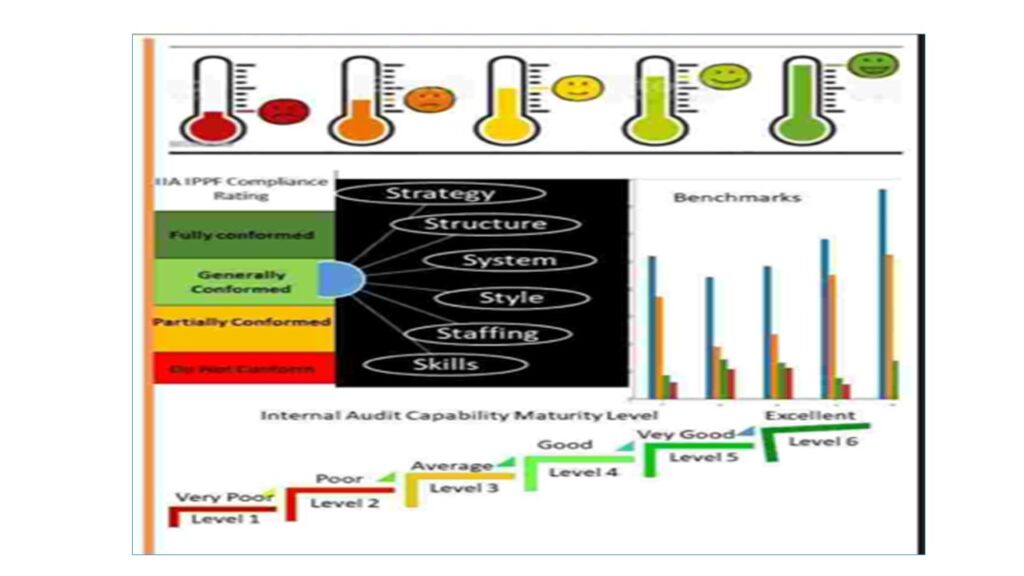

What are the major challenges with quality assessment reviews?

Experience has shown that most of the external quality assessments come with big surprises to the internal auditors, because of the failure of the internal audit to conduct internal self-assessment on its activities. The major contributing factors are:

- Knowledge gap of the right of the standard best practices, methodology and reporting styles.

- Fear of losing credibility and respects of the auditees, colleagues and bosses. The internal auditors enjoy auditing others and make a living out of the work but hate to be audited.

What are the key activity steps involved in the quality assessment reviews?

The high-level summary of the key specific activities covered during the conduct of the Internal and external quality assessment reviews are -:

- Phase 1 – Engagement planning

- Phase 2 – Validation of the business needs and stakeholder’s expectations.

- Phase 3 – Current state/AsIs status assessment

- Phase 4 – Root Cause Analysis

- Phase 5 – Reporting and stakeholders’ presentation

- Phase 6 – Development of Implementation Road Map

- Phase 7 – Implementation support

- Phase 8 – Post implementation support

Phase 1 – Planning requires completing the following activities:

- obtaining background information about the company

- confirming the key objectives for the reviews,

- developing the project plans,

- agreeing the key deliverables and stakeholders’ expectations from the quality review assignment,

- agreeing stakeholders to be interviewed.

- confirm the communication protocols, roles, responsibilities, timeframes, scope of work, assumptions and the critical success factors.

Phase 2 – Confirm business needs and stakeholders’ expectations involves understanding the perceptions and perspectives on the internal audit function. by various stakeholders in the organisation. These include the Directors of the Board, Board Committee members, Executive management, Senior Management levels, Midde management levels, selected operational lower level auditees, internal auditors and selected external business relationships such as the external auditors and consultants.