What should the quality assessment reviews cover?

Assessing the performance of the internal auditors goes beyond the assessment of the individual internal auditors. The Institute of Internal Auditors (IIA) mandates that the assessment requires a holistic approach by assessing the service delivery quality of the entire internal audit function. The Institute of Internal Auditors (IIA) is the global organisation that regulates the internal audit profession and practices across the globe. The top three quality measurement standards and tools that the IIA has prescribed for the quality assessment of the internal audit functions are:

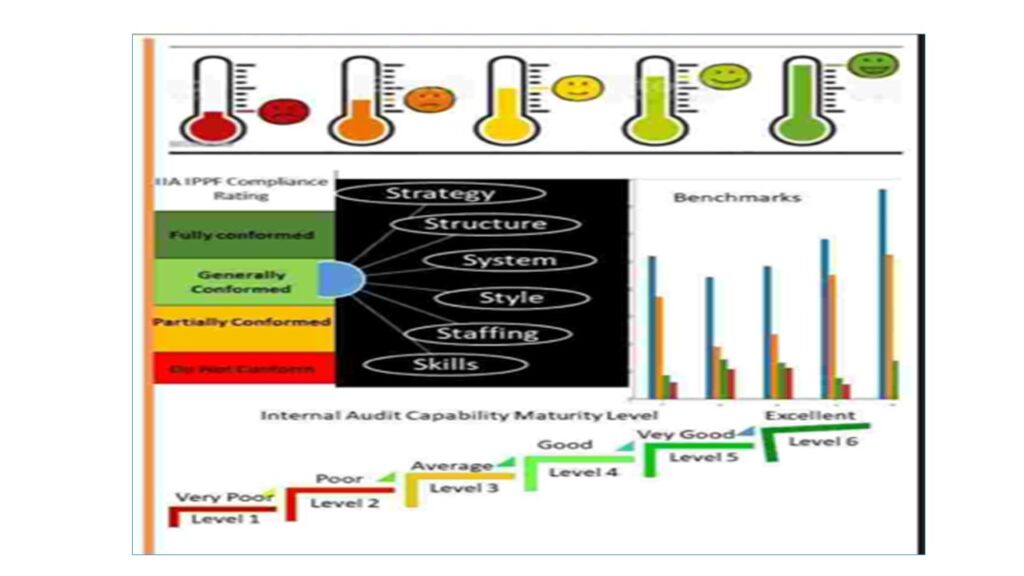

- IIA International Professional Practice Framework (IIA IPPF) Standard).

- IIA Internal Audit Capability Maturity Model (IIA IC-MM).

- IIA Audit Intelligent Suite (Formerly Gains Benchmarking Survey Study).

The IIA IPPF review is done to establish the conformance of the internal audit function to the IIA IPPF Standards and other applicable regulations. The IIA Internal Audit Capability Maturity is done to determine the extent of impacts and value contributions of the internal audit function in achieving the overall corporate strategic goals and objectives while the IIA Audit Intelligent Suite review is done to compare the internal audit performance with the industry standards, specific leading practices organisations and peers.

Each of the above IIA quality measurement standards and tools provides specific focus areas to be reviewed and analyzed about the internal audit service delivery. The reviews of the focus area help the reviewers or quality assessor to achieve the following:

- gain robust insight into what the internal audit service delivery is at each of the focus areas in terms of the gaps, strengths and improvement opportunities.

- provide at the aggregate level the bigger picture of the overall performance of the Internal Audit function.

- strengthen the internal audit’s ability to direct the time and effort of its human capital to optimize the resources and full value of the internal audit potentials.

- form basis for drawing conclusions and giving opinions on the internal audit performance against the measurement standards and stakeholders expectations,

- providing actionable recommendations and advice to move the internal audit function to the desired performance levels.