Why EQA Matters.

EQA matters because the internal audit function must be audited just like they audit the corporate governance, business management (core and support) units and Second Line of Defense functions.

EQA simply means auditing the internal auditor and it is necessary to assess how well they are doing in fulfilling the Value Protection and Value Addition Mandates to their organizations and stakeholders.

EQA should not be perceived as a CHECKLIST or ACADEMIC EXCERCISE to meet regulatory compliance. They must be used as a strategic tool to reposition the Internal Audit position to deliver the balance the delivery of Value Protection and Value Addition.

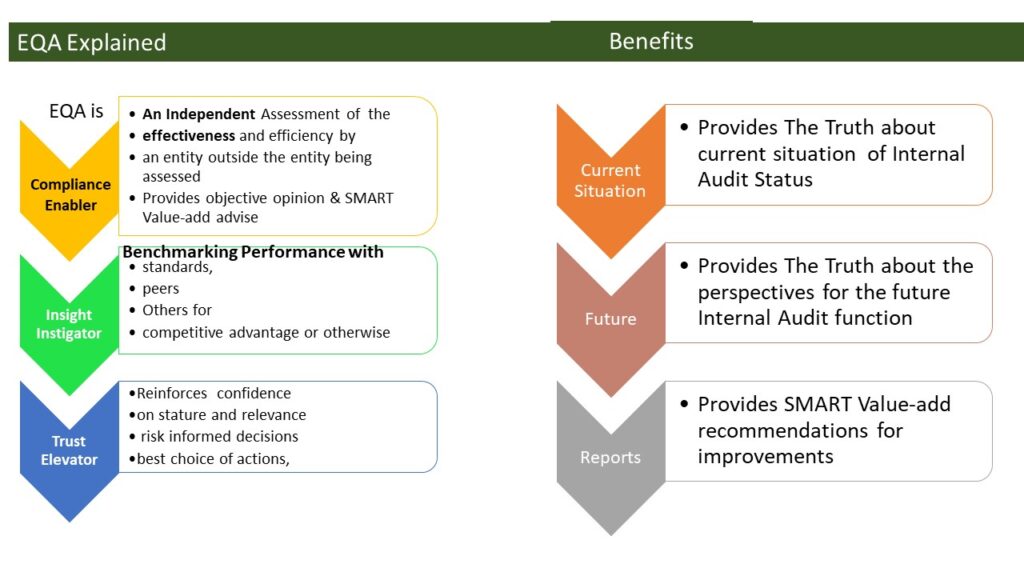

The additional benefits of EQA are presented below.:

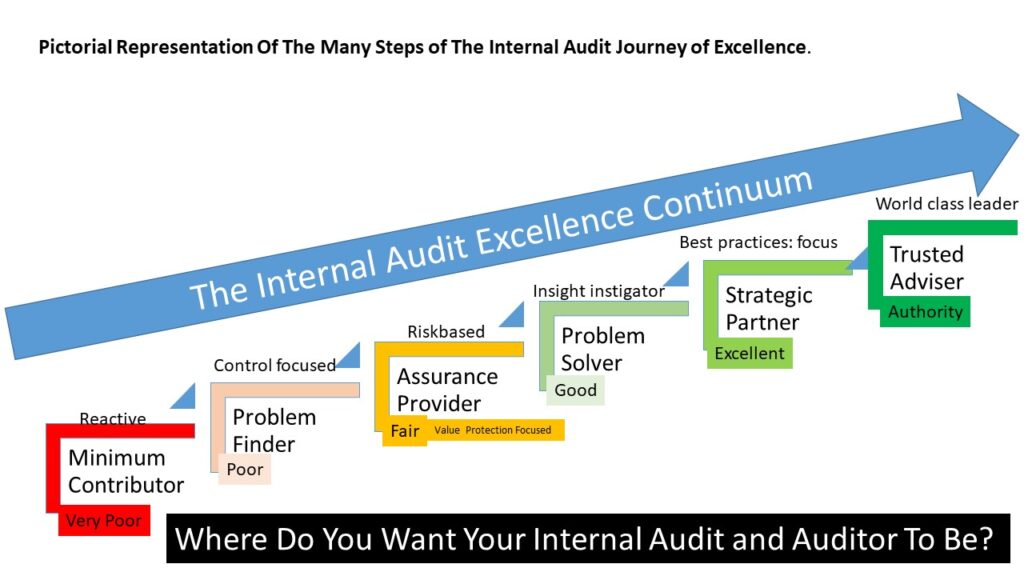

Using EQA as a strategic tool requires understanding that Internal Auditing is a journey of Excellence with a starting point and steps in between but with no fixed ending point.

Below is the pictorial representation of the Internal Audit Excellence Continuum depicting the starting points, steps in between and no fixed end.

EQA Focus Review Areas:

EQA focuses its review on the Internal Audit Management Life Cycle by checking the quality of the design, execution and monitoring of the various levers enabling internal audit performance. Some of the key areas covered are as follows:

- Internal Audit strategy -methodologies and tools adopted and basis for gathering business priorities, and leveraging business risk events (risk registers) for developing risk based internal audit plans.

- hierarchical reporting structure or authorities’ levels with the internal audit function – internal audit governance and management teams,

- Systems – internal audit policies, processes and SOPs, mandates, internal audit charter, planning templates, working papers documentations and reporting templates.

- Skills — Competency frameworks (technical & soft skills) & availabilities within internal audit function.

- Staffing Capabilities – staff mix and numbers within the internal audit function and recruitment ap

- Staff – Talent acquisition and retention of internal audit staff -recruitment criteria, staff development, promotions and out counselling

- Stakeholders’ engagement style – communication and interactions with Auditees, Executive Management and Boad adhering to the 7C effective Communication Principles.

- Shared Values – alignment of internal audit core values and practices with the overall corporate shared values and culture.

Very insightful and helpful.

Thanks for what you are doing

Thanks you very much Chileobim for your inspiration. I appreciate